My Trading Game Plan Revealed - 07/14/2026: CPI Shockwave Lowers Fed Odds, IBM Plunge Fuels Memory Chip Rally

Cooler Inflation Lifted Markets, but the Charts Still Have to Confirm It

The cooler CPI report changed the macro setup immediately. Treasury yields pulled back, the US Dollar weakened, and risk assets caught a bid. But Gareth Soloway’s central message from this morning’s My Trading Game Plan Revealed was not that one inflation report had cleared the path higher.

The market received a better catalyst. It has not yet delivered technical confirmation.

That difference is especially important in a market where the major indices remain between support and resistance, IBM is suffering one of its sharpest declines in years, and capital is rotating aggressively into the memory-chip companies benefiting from the artificial-intelligence spending cycle.

Lower Yields Give Equities Breathing Room

The CPI data came in cooler than expected across several important measures, reducing pressure on the Federal Reserve to tighten policy further. The immediate transmission mechanism was visible in the bond market.

The 10-year Treasury yield had recently rallied from trendline support near 4.36% to an overnight high around 4.64%. After the inflation release, it pulled back toward 4.56%. That decline matters because elevated yields have been one of the primary constraints on equity valuations.

The US Dollar also reversed lower from resistance. A softer dollar can support multinational companies by increasing the translated value of overseas revenue, but the more immediate market signal is broader: falling yields and a weaker dollar remove two sources of pressure from risk assets.

That creates a more constructive backdrop. It does not guarantee that stocks break higher.

The S&P 500 Is Still Waiting for a Decision

The broader market remains caught between clearly defined technical boundaries. Gareth described this as a form of market purgatory, with price trading between meaningful support below and resistance above.

The important point is not the exact middle of that range. It is that the index has not reached either area where the risk-reward becomes more attractive.

Trading aggressively in the middle of a range often means accepting poor positioning. Support offers a level where fear may become overextended. Resistance offers a level where optimism may have moved too far. Between those points, the market can generate movement without producing a clean setup.

The CPI report improved the probability of an upside resolution, but price still has to prove it. Until the index clears resistance or returns to support, patience remains part of the game plan.

IBM Reveals Where Corporate Spending Is Moving

The more important development beneath the index was the divergence inside technology.

IBM fell sharply after warning that customers were directing more of their budgets toward memory chips and other artificial-intelligence infrastructure needs. The headline suggested weakness in IBM’s data-center business, but Gareth’s interpretation went one level deeper.

The spending may not be disappearing. It may be moving.

Companies have limited capital-expenditure budgets. As demand for memory and AI infrastructure accelerates, spending allocated to legacy technology projects can be delayed or reduced. That creates a sharp divide between the companies losing budget share and those receiving it.

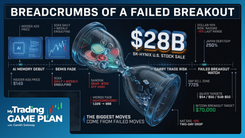

IBM’s decline brought the stock directly into a major rising trendline connecting several important pivot lows. That support was near $218, with the stock briefly trading around $217 before stabilizing.

After a decline of roughly 25% from peak to trough, the chart offered a potential mean-reversion setup. Gareth acquired shares near $221 while looking for a rebound above $230. The trade was based on technical support and the scale of the selloff, not on an assumption that IBM’s fundamental problems had disappeared.

The risk is straightforward. A bounce can develop as long as the macro trendline holds. A decisive break below it would weaken the setup and suggest that the market is pricing in something more serious than a temporary spending delay.

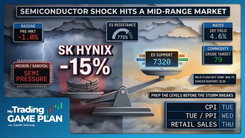

Memory Chips Are Receiving the Other Side of the Rotation

The companies benefiting from the spending shift moved in the opposite direction.

Strength in SK Hynix helped lift US-listed memory names, including Micron and Sandisk. Both produced large swings as traders repositioned around the idea that AI spending remains strong but is becoming increasingly concentrated.

This is why the technology sector cannot be treated as one uniform trade. IBM’s decline and the strength in memory stocks are part of the same story. One group is losing near-term budget priority while another is absorbing the capital.

That divergence is more useful than the headline question of whether technology was broadly higher or lower. It shows where institutions believe the strongest demand remains.

Bank Earnings Reinforce the Importance of Positioning

The bank reactions delivered the same lesson from a different angle: strong earnings do not automatically produce higher prices.

Goldman Sachs rallied as underwriting and capital-markets activity supported results. JPMorgan traded lower despite a strong quarter after entering the report near record highs and printing a major topping tail. The difference was not simply the quality of the earnings. It was how much optimism each chart had already priced in.

Bank of America entered the session with a more constructive pattern after breaking above the neckline of an inverse head and shoulders formation. That structure produces a projected area near $64 to $65, although the breakout still needs to hold.

The broader takeaway is that earnings are catalysts, not complete trading frameworks. The reaction depends on valuation, positioning, chart structure, and whether the results were strong enough to exceed expectations already embedded in price.

Gold, Oil, and Bitcoin Still Need Closing Confirmation

Outside equities, several major assets also reached decision points.

Gold bounced after testing the $4,000 area, but the closing candle matters more than the morning rebound. A close near the upper portion of the day’s range would support the case for a sustained recovery. A weak close would show that buyers could not maintain control even after receiving a favorable inflation catalyst.

Oil has already pushed through its initial target near $79 as tensions surrounding the Strait of Hormuz continue to support prices. The next technical reference is the gap near $84, followed by larger resistance around $87.

Bitcoin also rallied after the CPI release, but the breakout level remains near $64,000. A confirmed daily close above that area would strengthen the bullish structure. Failure to close above it would leave Bitcoin inside the same consolidation despite the intraday enthusiasm.

Bottom Line

The CPI report improved the macro environment by lowering yields and weakening the dollar, but the market is still demanding confirmation from price.

The index remains between major technical boundaries. IBM is testing whether long-term support can produce a mean-reversion bounce. Memory-chip companies are showing where AI-related capital is still flowing. Banks, gold, oil, and Bitcoin are all reinforcing the same message: the catalyst creates movement, but the close determines whether the structure actually changed.

The game plan is not to chase the first reaction. It is to identify where the market confirms it.

Trading involves substantial risk. All content is for educational purposes only and should not be considered financial advice or recommendations to buy or sell any asset. Read full terms of service.