My Trading Game Plan Revealed - 07/15/2026: IBM Shockwave, S&P Trendline and Yen Carry Trade Risk

IBM’s Historic Selloff Exposes the Leverage Risk Beneath a Rising S&P 500

IBM’s 25% collapse was the most important signal from this morning’s market, but not because one legacy technology company disappointed investors. The size of the decline showed what can happen when crowded positioning, limited institutional cash, and forced deleveraging meet even a modest negative catalyst. That warning arrived while S&P 500 futures continued higher following cooler inflation data, creating a market where the index structure still looks constructive even as the risks beneath it become harder to ignore.

That contrast defined Gareth Soloway’s framework on today’s My Trading Game Plan Revealed. The broader market has not broken, and the major technical levels remain intact. At the same time, IBM demonstrated how quickly selling can accelerate when investors are already fully committed and have little liquidity available to absorb a shock. The lesson was not that one earnings warning predicts a broader collapse. It was that the current market may be more fragile than the major indexes suggest.

IBM’s Decline Was About More Than Earnings

IBM’s warning came in below expectations, but the size of the miss did not appear to justify a decline of roughly 25% on fundamentals alone. The stock suffered its largest one-day drop on record, falling into a support zone between approximately $215 and $218. That area mattered because it aligned with long-term technical support already visible on the chart before the earnings news arrived.

Gareth’s read was that the move reflected forced liquidation as much as a reassessment of IBM’s business. When institutional investors are heavily invested and carrying limited cash, a negative catalyst can trigger margin pressure, risk reductions, and algorithmic selling. Once that process begins, price can move far beyond what the initial news would normally imply because sellers are responding to liquidity needs rather than valuation.

That interpretation is reinforced by reports that hedge-fund cash exposure is near historic lows. The exact figure requires confirmation before publication, but the broader point remains relevant: institutions have less capital available to absorb sudden selling when portfolios are already fully deployed. IBM became a real-time example of how leverage can amplify a manageable disappointment into a much larger technical event.

The chart now defines the next phase. The $215 to $218 zone is the support area that stopped the initial decline, while the prior pivot near $240 to $244 becomes the first major resistance zone on a reflex bounce. A recovery into that area would not erase the breakdown, but it would be consistent with the type of retracement that often follows a forced-liquidation event. A failure to hold the support zone would keep the larger breakdown in control.

The S&P 500 Structure Has Not Broken

IBM’s collapse did not immediately spread into the broader market. S&P 500 futures moved higher after the Producer Price Index came in below expectations, reinforcing the view that inflation pressures may be cooling. The important point, however, was not the initial reaction to the data. It was that the index remained inside the same technical structure that has governed the market for months.

The S&P 500 is trading between major resistance near 7,725 and support near 7,325. Within that range, the most important feature is the long-term trendline connecting prior major highs. That line has been tested repeatedly, and each test has attracted buyers. As long as the index continues to hold above it on a closing basis, the broader bullish structure remains intact despite the weakness developing beneath the surface.

Repeated tests also create risk. Every additional approach places more pressure on the same level, and a confirmed break could trigger a faster move as systematic traders respond to the loss of support. Gareth’s downside framework places 7,000 as the next major area if the trendline fails and selling accelerates. That is not the active setup while support holds, but it is the level that becomes relevant if the current structure gives way.

The market is therefore not at a confirmed turning point. It is at a point where confirmation matters. IBM exposed the vulnerability created by leverage, but the S&P 500 has not yet validated that warning through a structural breakdown. Until that happens, the index can continue higher even while individual stocks experience severe dislocations.

Yields and the Yen Are the External Risks

The bond market delivered a more cautious signal than equities. Despite softer inflation data, the 10-year Treasury yield pulled back only modestly and continued to hold near its long-term trendline. If the market believed inflation had been fully neutralized, yields would likely be responding more aggressively. Their relative stability suggests that bond investors still see a risk of persistent inflation or a prolonged period of elevated interest rates.

That matters because higher yields continue to pressure equity valuations, particularly in technology and other long-duration assets. The risk is not a single move in the 10-year yield. It is the failure of yields to break lower even when inflation data provides a favorable catalyst. As long as the trendline holds, the bond market is not confirming the most optimistic equity-market interpretation of the data.

USD/JPY presents a separate but related risk. The pair is pressing into historically elevated territory while forming a large rising wedge. A similar setup in 2024 preceded intervention and a rapid unwinding of the yen carry trade. Because that trade often involves borrowing in yen to purchase higher-yielding assets elsewhere, a sudden strengthening of the yen can force leveraged positions to close across global markets.

The immediate signal has not triggered, but the setup deserves attention because of how quickly the transmission can occur. A sharp reversal in USD/JPY would not remain isolated to the currency market. It could pressure US technology stocks, raise volatility, and accelerate the type of forced selling already visible in IBM. The yen is therefore less important as a standalone chart than as a potential source of broader liquidity stress.

Semiconductor Divergence Adds Another Warning

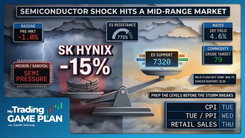

The semiconductor sector is also beginning to show uneven participation. SK Hynix surged more than 25%, but comparable memory names posted much smaller gains. Micron, Sandisk, and Seagate all moved higher, yet none confirmed the strength of the sector leader. That divergence suggests investors may be rotating between individual names rather than increasing exposure to the entire group.

The muted response matters because strong sector moves are more reliable when multiple leaders participate. When one stock surges while related names lag, the move may reflect company-specific positioning rather than a durable change in sector demand. The same caution appeared in ASML, which reportedly delivered strong earnings but struggled to hold its early gains.

The market is also beginning to weigh whether software efficiency could reduce future demand for memory hardware. Reports that AI tools may lower memory requirements are still developing and should be verified carefully, but the concept has clear implications. If software allows companies to achieve similar performance with less hardware, some of the long-term demand assumptions supporting memory valuations may need to be revised.

None of this confirms a major semiconductor top. It does show that strong headlines are no longer producing equally strong follow-through across the group. That changes the read because leadership is narrowing at the same time leverage and interest-rate risks remain elevated.

The Framework Remains Probabilistic

Natural gas provided the clearest reminder that even well-formed technical patterns can fail. The chart had developed a cup-and-handle structure, which normally supports a bullish interpretation, but price broke lower instead. The failed setup did not invalidate technical analysis. It demonstrated why patterns must be treated as probability frameworks rather than guarantees.

A pattern becomes more useful when additional factors support it. Fibonacci levels, moving averages, gap fills, and established support zones can improve the quality of a setup, but no combination eliminates risk. The job is not to predict every move correctly. It is to define where the setup works, where it fails, and how much exposure is appropriate before the outcome is known.

That same framework applies to IBM and the S&P 500. IBM’s support zone creates the possibility of a reflex bounce, but it does not guarantee one. The S&P trendline remains constructive, but it is not permanent. USD/JPY presents a potential carry-trade risk, but that risk remains conditional until the chart confirms a reversal.

Bottom Line

The central message from today’s market was not that IBM’s collapse will automatically spread to the major indexes. It was that the decline revealed how quickly leverage can transform a modest disappointment into forced liquidation. That warning matters because the S&P 500 is still holding its structure while yields remain firm, semiconductor participation narrows, and USD/JPY approaches a level associated with prior carry-trade stress.

The market remains technically constructive as long as the S&P 500 holds its long-term trendline and the 7,325 support area. A confirmed break would shift the focus toward 7,000 and raise the probability that the liquidity pressure seen in IBM is becoming a broader market event. Until then, the index trend and the underlying risks are sending different messages, and traders need to respect both.

Trading involves substantial risk. All content is for educational purposes only and should not be considered financial advice or recommendations to buy or sell any asset. Read full terms of service.