My Trading Game Plan Revealed - 05/27/2026: Semiconductor Concentration And Market Breadth Warning

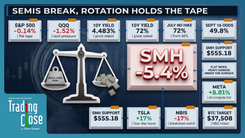

The S&P 500 is making higher highs. Gold is breaking down. Silver is breaking down. Bitcoin sold off yesterday while equities closed green. Equal-weight indices are lagging badly.

That combination does not describe a healthy risk-on market. It describes a market being carried by a very small number of very large stocks — and everything underneath is quietly telling a different story.

That is the read Gareth Soloway laid out in this morning's My Trading Game Plan. The semiconductor sector has reached a concentration level that is actively masking deteriorating breadth. When that concentration breaks — or even wobbles — there is no broad market underneath to absorb it.

The Breadth Problem Nobody Is Talking About

The S&P 500's cap-weighted index keeps grinding higher. The equal-weight version is lagging significantly. That gap is the tell.

In a healthy bull market, participation is broad. When six semiconductor stocks account for the majority of index-level gains, the rally becomes fragile in a very specific way — it looks fine until it doesn't, and then the rotation has nowhere to go.

The semiconductor market caps speak for themselves: Nvidia at approximately $5.2 trillion, Taiwan Semi and Broadcom at $2 trillion each, Micron and SK Hynix both crossing $1 trillion, AMD at approximately $800 billion, Intel at approximately $620 billion. These are not sector weights — they are the market. And Nvidia, despite the sector ripping higher, actually closed down yesterday. Either money is rotating into other chipmakers, or institutional holders are beginning to distribute after earnings. One of those is a rotation. The other is an exit.

Walmart is adding to the picture. The stock is falling sharply — not because it is a boring business, but because the company's latest earnings call raised direct warnings about the health of the consumer. A struggling consumer and multi-trillion-dollar AI valuations running simultaneously is not a tension that resolves quietly.

What the Global Charts Are Saying

The breadth warning is not just domestic.

South Korea's KOSPI surged on SK Hynix crossing $1 trillion — then printed a massive topping tail. That matters because Samsung Electronics and SK Hynix together make up more than 50% of the KOSPI 200 index. A bearish reversal signal on a two-stock index is not a technical footnote. It is the signal.

Japan's Nikkei 225 closed back below its key trend line. Taiwan's market cap now exceeds India's — an island nation outvaluing a country of over a billion people, driven entirely by one semiconductor company. That is not a valuation story. That is a concentration risk story wearing valuation clothing.

The S&P 500's own daily chart has printed consecutive topping tails over the last two sessions — buyers pushing to intraday highs, sellers driving price back near the open by the close. The trend is still technically intact. But consecutive topping tails on the most vertical weekly run of this cycle is the market starting to show its work.

"Investors are programmed more and more to just believe every dip you just buy it. And I've seen the comments out there saying the markets will never go down again because the president will never let it go down again."

That level of complacency is not a contrarian signal on its own. But it is exactly the psychological backdrop that was present at the peak of the dot-com cycle. The professional response is not to short a rising market — it is to wait for a definitive change in character. Specifically: a lower low.

The Institutional Playbook at Peak Euphoria

Late-stage bull markets have a consistent pattern. Analyst targets get disconnected from fundamentals. Retail gets large IPO allocations. Institutions get liquid.

The UBS action on Micron is a clean example. The previous price target was $535. The new target is $1,625 — justified by comparing Micron's PE to Nvidia's. Nvidia designs proprietary chips the U.S. government restricts from export to China. Micron makes memory — a commoditized product that has been around since the dot-com era. Assigning a proprietary tech multiple to a commodity memory manufacturer is not a research call.

"An analyst from UBS comes out and says, hey, I want to make a name for myself. So let me give Micron this crazy valuation or price target of $16.25… their former price target was $525. So they basically tripled it, over tripled it."

The SpaceX IPO is running a similar dynamic. Historically, when an asset is genuinely scarce and high-quality, institutions keep the allocation. Large retail allocations are not generosity — they are distribution.

"When these valuations get this wacky — institutions are like, thank goodness, let's dump, dump, dump, dump, dump to retail. And there it goes."

The Divergence That Cannot Be Explained Away

The cross-asset breakdown is the hardest part of the current market to ignore.

Gold has formed a textbook bear flag and is actively breaking down. Next major downside target: $4,100. Silver is under its trend line with a downside target between $64 and $66. Bitcoin sold off hard yesterday while equities were green — and is seeing further downside today. The critical level to watch is the lower trend line support near $73,000. A break there does not stay contained to crypto.

The only commodity supporting the equity narrative is oil, which continues to drop on Strait of Hormuz optimism. Lower oil keeps inflation expectations in check, which keeps yields from spiking, which keeps equity algorithms in buy mode. That is a real and functional relationship. It is also a single variable holding a lot of weight.

When gold, silver, and Bitcoin are all breaking down simultaneously while equities make new highs, the message is not ambiguous. These are the assets that lead in genuine risk-on environments. Their breakdown while equities run is either a massive rotation into pure equity risk — or it is an early warning that the equity move is running on a narrower foundation than the index level suggests.

ZS Scaler and CrowdStrike: Where the Setups Live Today

Earnings continue to create specific, actionable levels regardless of the macro backdrop.

ZS Scaler is falling sharply on earnings, pulling CrowdStrike down with it. The gap fill sits at $138. The high-probability zone is lower — $130.60 is the level. Any price action below $131 is the entry zone worth watching.

CrowdStrike has broken through an upsloping near-term trend line. The setup here is to wait for the rally back and retest of that broken trend line from underneath. The reaction at that retest tells you everything — reclaim or rejection dictates the next directional move.

Both setups follow the same principle: wait for price to come to a predefined level. Do not chase the breakdown. Do not buy the first dip. The level is the trade.

What to Watch

- S&P 500 lower low — The trend is intact until it isn't. The signal to watch for is the first lower low on the daily chart. Until that prints, the trend is technically bullish and the short thesis has no trigger.

- Bitcoin $73,000 — The lower trend line support. A confirmed break below this level has cross-asset implications. This is the number.

- Gold $4,100 — The next downside target after the bear flag breakdown. Watch for either a flush to that level or a reclaim above the flag structure that negates the pattern.

- KOSPI and Nikkei — Two overseas charts flashing the same warning as domestic breadth. Watch whether the KOSPI topping tail follows through to the downside. If both Asian indices continue lower, the global semiconductor thesis is being tested at its source.

- ZS Scaler $130.60 — The high-probability entry zone. Below $131, the setup is active.

- Nvidia vs. the sector — If Nvidia continues to lag while other chipmakers run, the rotation thesis holds. If Nvidia starts to roll over and the sector follows, the breadth problem becomes a headline problem.

Trading involves substantial risk. All content is for educational purposes only and should not be considered financial advice or recommendations to buy or sell any asset. Read full terms of service.